US solar report 2025: Building a resilient workforce for America’s energy transition

How we got here

A decade ago, only three states had more than 1GW of installed solar capacity. Today, 33 states meet that threshold and the 248GW national capacity is enough to power 41 million homes.

This growth trajectory accelerated significantly after the Inflation Reduction Act passed in August 2022, bringing 30% investment tax credits, manufacturing incentives, and direct pay provisions that attracted over $100 billion in private investment.

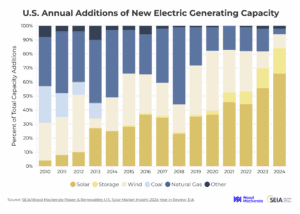

The results were immediate and substantial. Solar installations grew from 33.9GW in 2023 to nearly 50GW in 2024, accounting for 66% of all new electricity generation capacity. It’s the largest single-year addition by any technology in two decades. Domestic manufacturing expanded from 14.5GW to 42.1GW in just two years, with 51 new facilities announced. The industry seemed set for steady, predictable growth.

However, the One Big Beautiful Bill Act (OBBBA), enacted in July 2025, has altered these expectations.

Residential solar tax credit

The 30% residential solar tax credit will expire completely on December 31, 2025, with no phase-down period. This represents an accelerated timeline compared to the original IRA schedule, which planned to maintain the credit through 2032. To qualify for the full credit, homeowners must have their solar systems fully installed and commissioned by the end of 2025.

Commercial and utility-scale solar credits

For commercial solar projects, the timeline is tighter but more forgiving:

- Projects that begin construction by July 4, 2026 remain eligible for the full 30% Investment Tax Credit.

- Projects must be placed in service by December 31, 2027 to receive any federal solar tax incentive.

- A July 7, 2025 executive order directs the Treasury to tighten definitions for “beginning construction” mandating substantial onsite physical work rather than minimal upfront activity.

Advanced manufacturing credits

The OBBBA phases out the advanced manufacturing production tax credit for wind components sold after December 31, 2027, while solar and battery components continue to receive manufacturing credits through 2029.

The new deadlines force companies to rethink their workforce strategies for both immediate needs and long-term sustainability.

The 3 forces reshaping America’s solar workforce

Even before the policy swings, 44% of solar employers reported hiring difficulties, especially in construction roles. The issue extends beyond simple labor shortages to finding workers with the right skills for increasingly complex projects. Now, three factors are converging to create unique workforce pressures. Understanding each is essential for developing effective talent strategies.

- The July 2026 construction deadline is accelerating project timelines across the industry. Developers are advancing projects originally planned for 2027-2029 to qualify for expiring incentives. Our analysis suggests annual installations could reach 60-70GW in 2025-2026 as companies work to meet deadlines, up from the already record-breaking 50GW in 2024.

- Interconnection delays continue to constrain project completion. Currently, 1,086GW of solar projects await grid connection approval—more capacity than the entire US electricity system. With average wait times now exceeding five years and only 14% of queued projects historically reaching completion, developers are pursuing multiple projects simultaneously to ensure some succeed. This parallel development approach significantly increases near-term workforce requirements.

- New supply chain requirements add complexity to project planning. Foreign Entity of Concern restrictions mandate 40-60% non-Chinese content by 2030. With US modules costing $0.31 per watt versus $0.10 globally, and domestic cell production at just 2GW, projects require more sophisticated supply chain management and compliance expertise.

Looking forward and navigating fluctuating demand

The most striking aspect of current workforce projections is their variability. Unlike typical industry growth patterns, solar employment needs will likely fluctuate significantly over the next five years.

In 2025-2026, we’re seeing a period of accelerated growth to support 60-70GW of annual installations. The industry needs approximately 355,000 workers by 2026 to support this, up from 279,447 today (Dec 2023 data). Current hiring trends suggest we’ll reach only 302,000 workers by then, leaving a gap of 53,000 positions. This represents the industry’s most acute near-term challenge, particularly for construction and installation roles.

In 2027-2028, we expect to see some market adjustment. When federal incentives expire, annual installations may decrease to 35-45GW based on simple economic competitiveness. This could reduce workforce needs to around 320,000, potentially leaving some workers hired during the expansion without full-time positions. Companies will need strategies to maintain critical talent while adjusting to lower activity levels.

From 2029-2030 we expect to see a new equilibrium. As the market stabilizes without subsidies, installations should settle around 38-40GW annually, supporting 310,000-325,000 workers. While below earlier projections of 420,000 jobs by 2030, this still represents solid employment in a maturing industry.

This variable demand pattern of growth, adjustment, and stabilization requires different thinking around workforce development than traditional “steady growth” scenarios.

How to build adaptive workforce strategies

Solar companies are already developing innovative approaches to manage these workforce variations. Their strategies offer practical lessons for the broader industry, including:

- Flexible staffing models: rather than relying entirely on permanent hires, successful companies are building mixed workforce models. They maintain core teams of permanent employees while developing relationships with qualified contractors who can support during peak periods. A renewables recruitment specialist like Taylor Hopkinson can support permanent team builds, while tapping into our pool of experienced contract specialists, which contains the most in-demand skillsets, when necessary.

- Regional deployment centers: the geographic mismatch requires creative solutions, with 29% of workers in California but major projects in Texas and the Southeast. Companies are establishing regional bases where workers live but from which they deploy to project sites for defined periods. This approach typically costs 15-20% more than local hiring but less than full-time travel positions, while improving worker satisfaction and retention.

- Accelerated training programs: traditional multi-year apprenticeships don’t match current timeline pressures. Companies are implementing focused 90-day training programs for specific skills, particularly electrical work and equipment operation. They’re recruiting from construction, manufacturing, and oil and gas sectors where workers have transferable skills, then providing targeted solar training.

- Career continuity planning: forward-thinking employers are already planning for post-2027 workforce needs. They’re creating pathways from construction to operations and maintenance roles, offering retention bonuses that vest after the 2027 transition, and cross-training workers in multiple disciplines to increase their versatility as market needs shift.

- Collaborative approaches: companies are forming partnerships that would have seemed unlikely before. The benefits can be varied, such as shared training facilities that reduce costs for all participants. Worker exchanges between regions with complementary seasonal patterns can maximize utilization, while joint recruitment initiatives expand the talent pool more effectively than competing for the same limited candidates.

Regional and skillset considerations

The workforce challenge varies significantly by region and role, requiring tailored approaches for different markets and positions.

California’s 80,000 solar workers represent deep expertise but high costs. Texas offers massive project pipelines (41GW planned) but limited local solar experience. Southeastern states provide lower costs and growing markets but need significant workforce development. Successful companies are building strategies that leverage each region’s strengths while addressing its limitations.

Skills requirements are also evolving. While basic installation skills remain important, the industry increasingly needs workers comfortable with battery storage integration, high-voltage systems, and sophisticated monitoring equipment. Project managers must understand both construction and complex regulatory requirements. Supply chain specialists need expertise in domestic content compliance and international logistics.

The most acute shortages exist in mid-level technical roles: electrical technicians, commissioning engineers, and quality control specialists. These positions require more than entry-level training but don’t necessarily need four-year degrees, making community college partnerships and certification programs particularly valuable. Solar installers earn median salaries of $51,860 annually, with the occupation projected to grow 42% through 2034, among the fastest growth of any profession.

The 2030 forecast for America’s solar industry

The next five years will test the solar industry’s ability to manage through policy-driven demand variations while maintaining quality, safety, and cost competitiveness. Success requires viewing workforce development not as a simple scaling exercise but as a strategic capability requiring continuous adaptation.

Recruitment professionals and HR leaders need to foster workforce flexibility, regional coordination, and skills acceleration. The companies that build adaptive workforce systems, capable of expanding for near-term opportunities while maintaining efficiency during slower periods, will emerge as industry leaders.

The data points to specific action items: closing the 53,000-worker gap by 2026, preparing for potential workforce reductions in 2027-2028, and building sustainable employment models for long-term growth. This isn’t just about meeting installation targets. It’s about building an industry that can thrive with or without subsidies.

America’s solar industry has demonstrated remarkable growth and resilience. Now it must prove it can manage through volatility while continuing its lead role in the nation’s energy transition. The workforce strategies we develop today will determine whether solar fulfils its potential as a cornerstone of American energy independence and economic growth.

-

View our latest solar vacancies in United States

-

Citations and sources

- Solar Energy Industries Association (SEIA) – Solar Market Insight Report 2024 Year in Review.

- Council on Foreign Relations – Congress’s ‘One Big Beautiful Bill’ Will Shrink Renewable Energy Investments. July 2025.

- SEIA – Solar Market Insight Report Q2 2025.

- Interstate Renewable Energy Council (IREC) – Census Solar Job Trends. Updated 2025.

- Lawrence Berkeley National Laboratory – Queued Up: Characteristics of Power Plants Seeking Transmission Interconnection. 2024.

- U.S. Bureau of Labor Statistics – Solar Photovoltaic Installers: Occupational Outlook Handbook. 2024-2025 Edition.

- Department of Energy – Tackling High Costs and Long Delays for Clean Energy Interconnection. 2024.

- National Renewable Energy Laboratory (NREL) – Solar Industry Update Q2 2025.

- Wood Mackenzie. – U.S. Solar Market Insight Q2 2025 Executive Summary.